…One would think that following two major market corrections of over 50% within the last two decades, investors would have a better appreciation for how much time it takes to compound your way out of losses. While buy-and-hold investors who stayed true to their strategy over the last two decades are indeed ahead, they lost many years of valuable compounding time in a quest to “get back to even.” The bottom line…is that corrections and crashes matter a lot.

investors would have a better appreciation for how much time it takes to compound your way out of losses. While buy-and-hold investors who stayed true to their strategy over the last two decades are indeed ahead, they lost many years of valuable compounding time in a quest to “get back to even.” The bottom line…is that corrections and crashes matter a lot.

The original article has been edited here for length (…) and clarity ([ ]). For the latest – and most informative – financial articles sign up (in the top right corner) for your FREE tri-weekly Market Intelligence Report newsletter (see sample here)

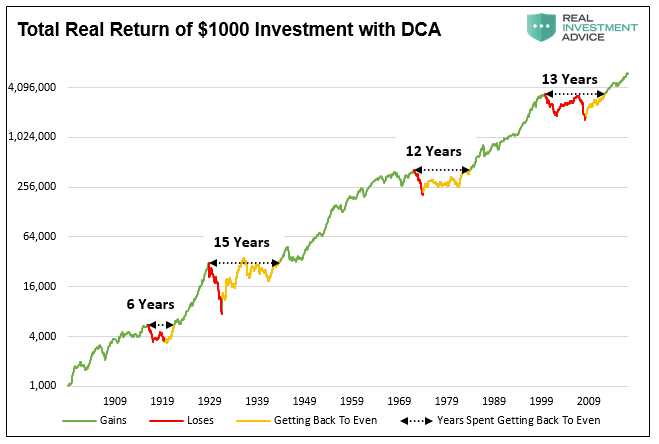

Just recently, Michael Lebowitz tweeted a chart that highlighted the issue of the time required to “get back to even.

The tweet, and graph was a simple reminder that markets spend a good deal of time declining and retracing those declines. These are long periods when investors are not compounding their wealth…

…The chart below shows the total real return (dividends included) of $1,000 invested in the S&P 500 with dollar cost averaging (DCA). While the periods of losing and recovering are shorter than the original graph, the point remains the same and vitally crucial to comprehend: there are long periods of time investors spend getting back to even, making it significantly harder to fully achieve their financial goals. (Note the graph is in log format and uses Dr. Robert Shiller’s data)

The…[charts above] expose several very important fallacies about the way many professional money managers view investing.

- The most obvious is that investors do NOT have 118 years to invest. Given that most investors do not start seriously saving for retirement until the age of 35, or older, most investors have just one market cycle to reach their goals.

- If that cycle happens to include a 10-15 year period in which total returns are flat, the odds of achieving their savings goals are massively diminished.

- If an investor’s 30-year investment cycle happens to end with a major market crash, the result was devastating. Time, duration and ending dates are crucially important to expected investor outcomes.

- Second and more importantly, “buy and hold” investors fail to consider risks, expected returns and alternative strategies.

- Consider that from 2000 through 2013, the S&P 500 Index, including dividends and inflation, delivered a zero rate of return.

- From 2000 through 2017, it returned a scant 0.30% more than risk-free Treasury bonds (5.4% annualized for stocks versus 5.1% annualized for bonds).

- Further, to reach that return it required the expansion of valuation multiples to extreme and risky levels. Equity investors have endured two 50% drawdowns, and over a decade of no returns, to achieve an 18-year, 30 basis point annualized pickup over bonds. In recent years that entailed holding equities that were well above long-term averages and presented a poor risk/return framework.

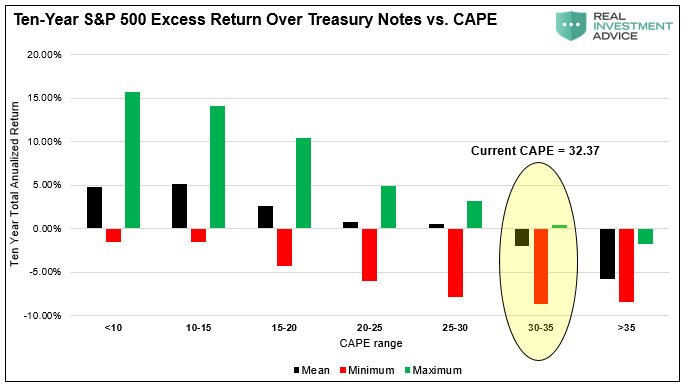

Given current valuations, it is possible, perhaps even likely, that we will wake up on New Year’s Day 2025 to a stock market that has lagged or only barely matched the return of bonds for a full quarter century. The chart below shows the annualized performance of 10-year equity returns versus 10-year U.S. Treasury notes based on over 100 years of history. Clearly equity investors will need to defy history to outperform risk-free bonds…

Summary – Part I

As shown and described, markets go through cycles. During these cycles, there are often incredible opportunities to own stocks. However, these cycles also include periods when risk should be minimized and greed should be constrained. Active management, unlike the static, one-size-fits-all mindset of the popular “buy and hold” strategy, seeks to measure risk and expected returns and invest in a manner in which one is aggressive when valuations are cheap, and defensive when they are rich. The philosophy of this approach seeks first to avoid large losses which are the key to compounding wealth.

The bottom line…is that corrections and crashes matter a lot. Avoiding losses weighs far more heavily in compounding wealth than does chasing returns…

Support our work: like us on Facebook, follow us on Twitter, or share this article with a friend. munKNEE.com – Voted the internet’s “most unique” financial site! (Here’s why)