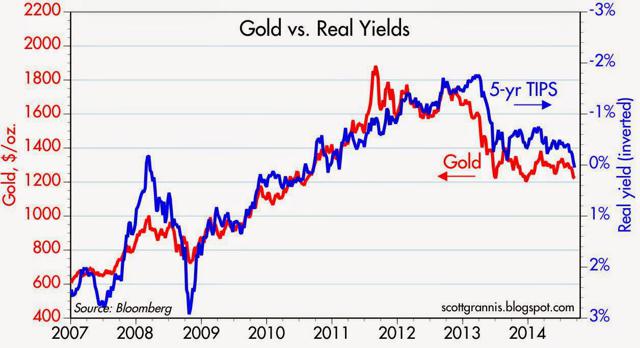

aversion and a somewhat improved economic outlook. There is no reason to fear the end of QE or the beginning of higher short-term interest rates. Let me explain further.

aversion and a somewhat improved economic outlook. There is no reason to fear the end of QE or the beginning of higher short-term interest rates. Let me explain further.

The following post is presented by Lorimer Wilson, editor of www.munKNEE.com (Your Key to Making Money!) and the FREE Market Intelligence Report newsletter (sample here). This paragraph must be included in any article re-posting to avoid copyright infringement.

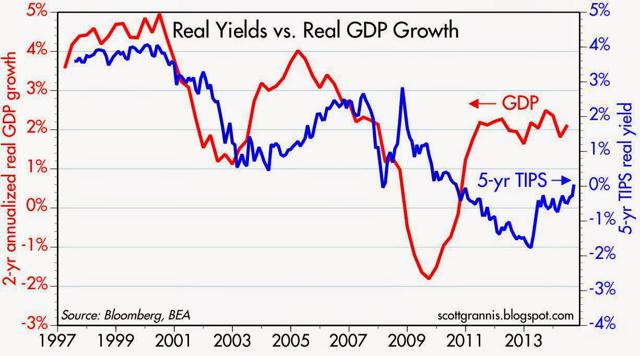

Real Yields vs. Real GDP Growth

The rise in real yields on TIPS also is a sign that the market’s outlook for economic growth is improving.

As the chart below shows, real yields tend to track the economy’s growth potential over the years, which makes a lot of sense. TIPS are unique because they offer a guaranteed real rate of return…Risk-free real return should be somewhat less than the expected real growth of the economy, since that is fundamentally uncertain, but real yields have been unusually low for the past few years (e.g., real yields have been -0.5%, whereas real economic growth has been a little over 2%), which I’ve taken to be a sign that the market was very pessimistic about the outlook for growth. That’s now beginning to change for the better, as real yields move higher. It’s not that the market has turned optimistic, however, it’s more accurate to say that the market now has become less pessimistic.

Editor’s Note: The author’s views and conclusions in the above article are unaltered and no personal comments have been included to maintain the integrity of the original post. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor.

If you liked this article then “Follow the munKNEE” & get each new post via

- Our Newsletter (sample here)

- Twitter (#munknee)

1. It’s Imperative That You Know ALL About Interest Rates! Here’s Why & How To Do So

I read hundreds of financial articles every week and most are nothing more than “financial entertainment” – unfounded forecasts, fear mongering or cheer-leading. That being said, there are a number of articles that are absolutely MUST READS if you are to become an informed investor and be in position to understand what is evolving in the financial environment and act accordingly. Introductory paragraphs and links to a number of them are provided in this post. Read More »

2. Borrowing Binge/Asset Bubble to Continue Until Real Rates Spike – Here’s Why

History strongly suggests that, rather than a return to a nice, placid world of “normal” interest rates, we are likely to see a continuation of the borrowing binge/asset bubble until real rates spike as a result of either soaring nominal rates soar or plummeting inflation. Here’s why that is the case. Read More »

3. What Does Current Money Velocity Say About A Future Rise In Interest Rates?

With all of the things in the world to worry about, how much should we worry about a sudden sharp increase in UST yields? The short answer is not much and here is why. Read More »

4. Will Higher Interest Rates Result From Additional Tapering?

After a long period of very low interest rates following the global financial crisis the central banks of the U.S. and U.K. are planning to gradually tighten their easy monetary policies as their economies improve. When their benchmark interest rates go up, interest rates elsewhere will go up to so should we worry if and when global financial conditions tighten? Read More »

5. We’re Doomed! Rising Interest Rates Will Cause Our Financial System To Implode

We’re doomed! Even if the economy were growing at a faster pace, it wouldn’t come close to offsetting the interest payments on our ever-expanding debt. As such, any sort of credit shock – either rising rates or a decline in the rate of debt expansion – will cause the system to implode. Let me explain why that is the case. Read More »

6. Interest Rates to Remain Low As Far As the Eye Can See? Perhaps, BUT

Everyone knows that interest rates are going to rise in the future so the real question is not whether they will rise, but when and by how much. [This article analyzes when that will most likely be.] Read More »

7. Higher Interest Rates Will Come Once These 4 Economic Conditions Are Met

4 economic conditions need to be in place for interest rates to rise ahead of – and independent of – the Fed’s forward guidance. The economy met only one of those conditions to date but will likely meet all four by the end of the year…What follows is a status report on the four conditions. Read More »

8. Interest Rates NOT Rising Any Time Soon – Even With Fed Tapering. Here’s Why

Everyone and their mom is expecting long-term interest rates to rise now that the Fed is tapering its bond buying programs. I have a couple of problems with this line of thinking because, although it seems like reducing demand for a security (i.e. tapering QE) would result in a drop in price, when you really think about how quantitative easing works this makes no sense and, secondly, the market is telling us this makes no sense. Let me explain. Read More »

9. What Affect, If Any, Will Rising Interest Rates Have On the Stock Market

The belief is that rising interest rates (as is currently occurring) are a sign that the economy is improving as activity is pushing borrowing rates higher. In turn, as investors, this bodes well for corporate profitability which supports the current valuations of stocks in the market. While this seems completely logical the question is whether, or not, this is really the case? Read More »

10. Rapid Rise In Interest Rates Will Collapse U.S. Financial System – Here’s Why

There is one vitally important number that everyone needs to be watching right now, and it doesn’t have anything to do with unemployment, inflation or housing. If this number gets too high, it will collapse the entire U.S. financial system. The number that I am talking about is the yield on 10 year U.S. Treasuries. Here’s why. Words: 1161; Charts: 2 Read More »

11. Don’t Worry About the Threat of Higher Interest Rates Hurting Stocks – Here’s Why

History clearly shows that stocks don’t fall during periods of rising interest rates. Sure, they might fall a little when a rate hike is announced – maybe for a week or so – but they usually bounce back quickly – and then they go higher. Read More »

12. Inflation Will Become a Huge & Growing Problem Beginning In 2015 – Here’s Why

A temporary period of deflation will result from the end of the Fed’s massive asset purchases followed by a period of inflation that will make the ’70s seem like an era of hard money. Here’s why. Read More »

13. High Inflation IS Coming – It’s Just A Question Of When – Here’s Why

There have been many econoblog posts of the form, “ha, ha, the people predicting inflation have been wrong so far, when will they give up?”. Let me try to explain why we know high inflation is coming eventually. Read More »

14. Tips from TIPS on Prospects for Growth, Outlook for Inflation & Future for Gold

TIPS are telling us that the market is quite pessimistic about the prospects for real growth, but not concerned at all about the outlook for inflation. Read More »

15. Runaway Inflation That Would Devastate USD Seems Unlikely – Here’s Why

Many investors are treating inflation as a certainty because the Fed has expanded its balance sheet to unheard of levels through its quantitative easing strategy. Some have even gone so far as to say that this program will utterly destroy the U.S. currency. To demystify this conclusion, I’m going to explain quantitative easing and why the Fed is using this monetary strategy. Afterward, I’ll explain why gold is still positioned to rise even if inflation continues to be low. Words: 786

16. Once Inflation Starts There Will Be NO Stopping It!

If inflation starts to head towards 5%, you can be sure it’s headed for 10% because they don’t have the ability to stop it now. The only antidote they have to the mess we are in, which is massively excessive debt reinforced by derivatives, is unlimited money printing. The idea that you can withdraw the punch bowl or sharply raise interest rates, it just doesn’t exist, unless you want to take a complete deflationary collapse.

17. What Causes Interest Rates to Rise? Is That Good or Bad?

Don’t get too worked up over interest on the national debt or what will happen when interest rates rise because, by then, we’ll likely be talking about ways to cool down the economy. [Why?] Because interest rates on US government debt are really a function of economic growth. If the economy is weak the Fed will pin short rates to stimulate the economy and if rates rise it’s going to be a function of better days ahead. Words: 525 Read More »

18. A Rise in Interest Rates Would Derail An Economic Recovery – Yes or No?

[While]… I am not currently predicting an acceleration in inflation [I believe]…that the risk of interest rate instability is very real [given that] core inflation is already above a key benchmark that the Fed has staked its credibility on,. It should be of concern to investors that, despite economic growth being so anemic and overall resource utilization being so low (including human resources), there is currently very little margin for error on the inflation front. [In this article the author evaluates the danger that rising interest rates could potentially have on the U.S. economy.] Words: 2050 Read More »19. Rising Interest Rates Could Plunge Financial System Into a Crisis Worse Than 2008 – Here’s Why

If yields on U.S. Treasury bonds keep rising, things are going to get very messy. What we are ultimately looking at is a sell-off very similar to 2008, only this time we will have to deal with rising interest rates at the same time. The conditions for a “perfect storm” are rapidly developing, and if something is not done we could eventually have a credit crunch.

20. Probability of Deflation Is 60%, Inflation Is 25% and Muddling Through Is 15% – Here’s Why

At the end of last year virtually every every single economist expected interest rates to rise this year as the Fed tapered their purchases and the economy improved but, in fact, interest rates on the 10 year U.S. Treasury have been going down year to date (from 3% to 2.5% after rising from about 1.6% to 3% last year). The masses, going along with this crowd, got fooled but we have been calling for a decline in interest rates for some time now due to world-wide deflation and it couldn’t be clearer to us that this is the most likely scenario for the United States. Let us explain. Read More »