Gold is in a tough situation right now. It is an enigma and it is suffering from an identity crisis. It does not know whether it wants to be a commodity or a currency…sometimes its price reflects its position as a commodity and other times as a currency. These days gold is struggling with both these roles…and when it decides what it wants to be there will be a price adjustment. I believe that adjustment is coming soon and that it will take the price lower. Here’s why.

from an identity crisis. It does not know whether it wants to be a commodity or a currency…sometimes its price reflects its position as a commodity and other times as a currency. These days gold is struggling with both these roles…and when it decides what it wants to be there will be a price adjustment. I believe that adjustment is coming soon and that it will take the price lower. Here’s why.

The above comments, and those below, have been edited by Lorimer Wilson, editor of munKNEE.com (Your Key to Making Money!) and the FREE Market Intelligence Report newsletter (see sample here – register here) for the sake of clarity ([ ]) and brevity (…) to provide a fast and easy read. The contents of this post have been excerpted from an article* by Andrew Hecht (technomentals.com/) originally entitled The Modern Gold Market – An Enigma and which can be read in its unabridged format HERE. (This paragraph must be included in any article re-posting to avoid copyright infringement.)

Gold & Inflation

The popular notion is that gold is the ultimate hedge against inflation. Gold is an asset; the question of whether it is a commodity or currency asset is what is bothering me these days. Gold must compete against other assets, and that is what determines its price. As a commodity, it is sensitive to the U.S. dollar, which is the international pricing mechanism for almost all commodities. When the dollar strengthens, gold generally moves lower and vice versa.

Gold & Interest Rates

Gold is also sensitive to interest rates; as real rates increase, gold must compete with other assets that offer a yield. The value of gold is constantly changing with human perception. Fear tends to be bullish for gold; a flight to quality in asset markets tends to increase its price. However, too much fear can also decrease gold’s value, as holders find themselves in a position where they must sell gold holdings to pay for losses in other assets. It is all very complicated, and the value proposition for gold has become even more difficult over recent years with the increase in “paper gold” or gold derivatives.

Paper Gold

…The amount of “paper gold” that trades far exceeds the amount of physical. Derivatives seek to reflect price movements in the physical, but one has to wonder if sometimes the tail is actually wagging the dog in the gold market…

I believe there is a pyramid in the world of gold investing and trading:

- At the top stands physical allocated gold, the purest form of ownership. Holders can pick up bars and coins, hold them in their hand, and marvel as the light reflects the lustrous glow of the beautiful metal.

- The next level on the pyramid is unallocated gold accounts and futures contracts. While both allow for the delivery of physical gold, there is a degree of risk in taking delivery. A bird in the hand is worth two in the bush when comparing holding a gold bar and holding a certificate or warrant representing a gold bar.

- The next steps down on the pyramid are options contracts and ETF and ETN products. These are often leveraged vehicles and while they have had an excellent correlation with movements in the price of gold over past decades, there are no guarantees that this will continue into the future. This makes these paper instruments further removed from the lustrous metal.

Today, the price of gold is a combination of action in all of these markets. That is because in order to hedge any paper gold transaction, a dealer or administrator must go back to the source, the physical gold itself.

…The advent of “paper gold” products has:

- increased market activity in gold as it has increased the addressable market for gold investment and trading…and

- increased liquidity for the metal. The proof of that is that in 1979-1980 when gold was moving higher towards its then peak at $850 per ounce, the bid/offer price spread for dealers widened to $5 at times. In 2011, when gold exploded to double the 1980 nominal highs, bid/offer spreads were far lower on both a percentage basis and nominal basis. This is because the gold market became larger and more liquid due to the introduction of these “paper gold” vehicles…

- improved liquidity, as demonstrated, and also

- increased price volatility.

I wonder if gold would have reached over $1,920 per ounce in 2011 if it were not for these new vehicles that brought more trend-following players to the market. I wonder if the price today would be higher or lower if these vehicles did not exist. My opinion is that gold would have never reached those dizzying heights in 2011 if it were not for the “paper gold” revolution – particularly the ETF and ETN products. While I do believe that quantitative easing and cheap money policies would have pushed gold to new all-time highs, the pinnacle actually reached was an extension due to a bullish herd mentality armed with these “paper” tools.

Gold Demand

Today, gold is $800 below the 2011 highs. There is clearly less interest in the gold market.

- The economic slowdown in China has probably decreased gold demand from the country that is the world’s number one consumer of all commodities by virtue of its sheer population (over 18% of the world) and its growth over recent years.

- It is human nature to flock to a bull market and hide from the bear. Commodity markets have been in bear markets since the 2011 highs; gold is not unique in that respect.

Gold Strength vs. Other Commodities

Gold has done pretty well when compared with other commodities, however. It is the strongest precious metal out there these days and it remains strong versus many, if not most, other raw material prices as well.

Gold vs. Silver & Platinum

…The silver-gold ratio is around around 76.7:1, and the discount of platinum under gold stands at $130 per ounce. Both of these represent substantial departures from mean historical levels over the past four decades in terms of these price relationships.

Gold vs. Copper and Crude Oil

Today, I want to look at two other commodities, copper and oil to see if gold is strong on a historical basis versus these raw material prices.

a) In the case of copper, divergence is present.

(click to enlarge)

The quarterly chart of the price of COMEX gold divided by the price of COMEX copper shows that there are approximately 483 pounds of copper value in each ounce of gold value today. As the chart above highlights, the swing point for this relationship dating back to the 1970s is around 375, which tells us that gold is expensive relative to the price of copper today.

b) The divergence between the price of gold and crude oil is even more glaring.

(click to enlarge)

Since the early 80s, the average number of barrels of NYMEX crude oil in each ounce of gold is around the 18 level. This relationship currently stands at over 24 barrels of crude oil value in each ounce of gold value. All of these divergences tell us that gold is strong. The question is, does strong mean overvalued or something else?

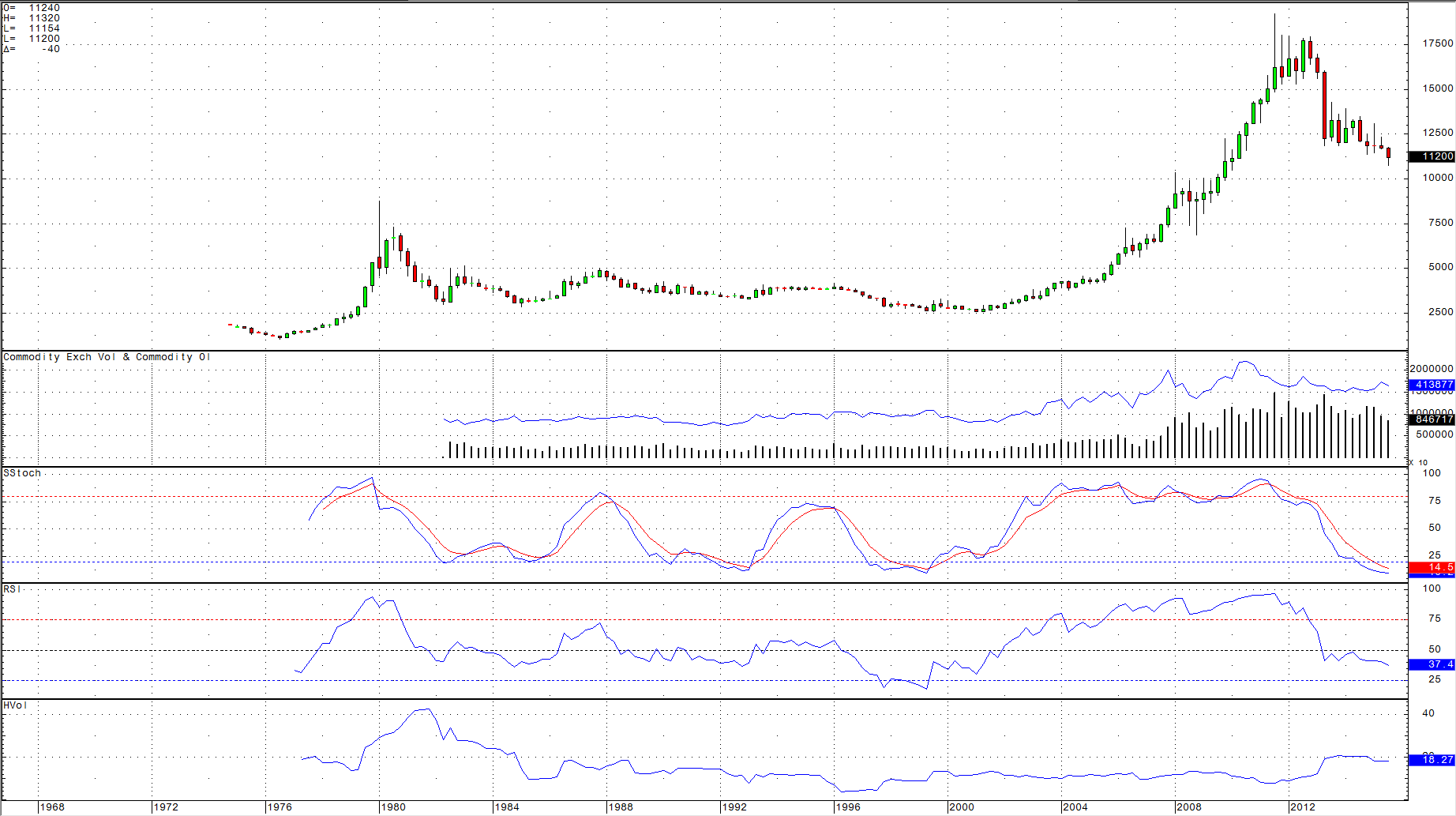

Gold’s Current Technicals

The current technical picture for gold on long-term charts is not pretty.

(click to enlarge)

Since 2011, the price of COMEX gold futures has been in a confirmed downtrend.

- While the slow stochastic, a momentum indicator, is in oversold territory,

- momentum still points lower.

- Open interest, the number of open long and short positions in COMEX gold futures contracts, stands at just under 414,000 contracts. Open interest is well below the highs of over 612,000 contracts in July 2010, but still considerably above pre-2007 levels. This is likely because the advent of “paper gold” vehicles, ETF and ETN products, have increased volume and interest in the gold market due to the ease of availability of these products.

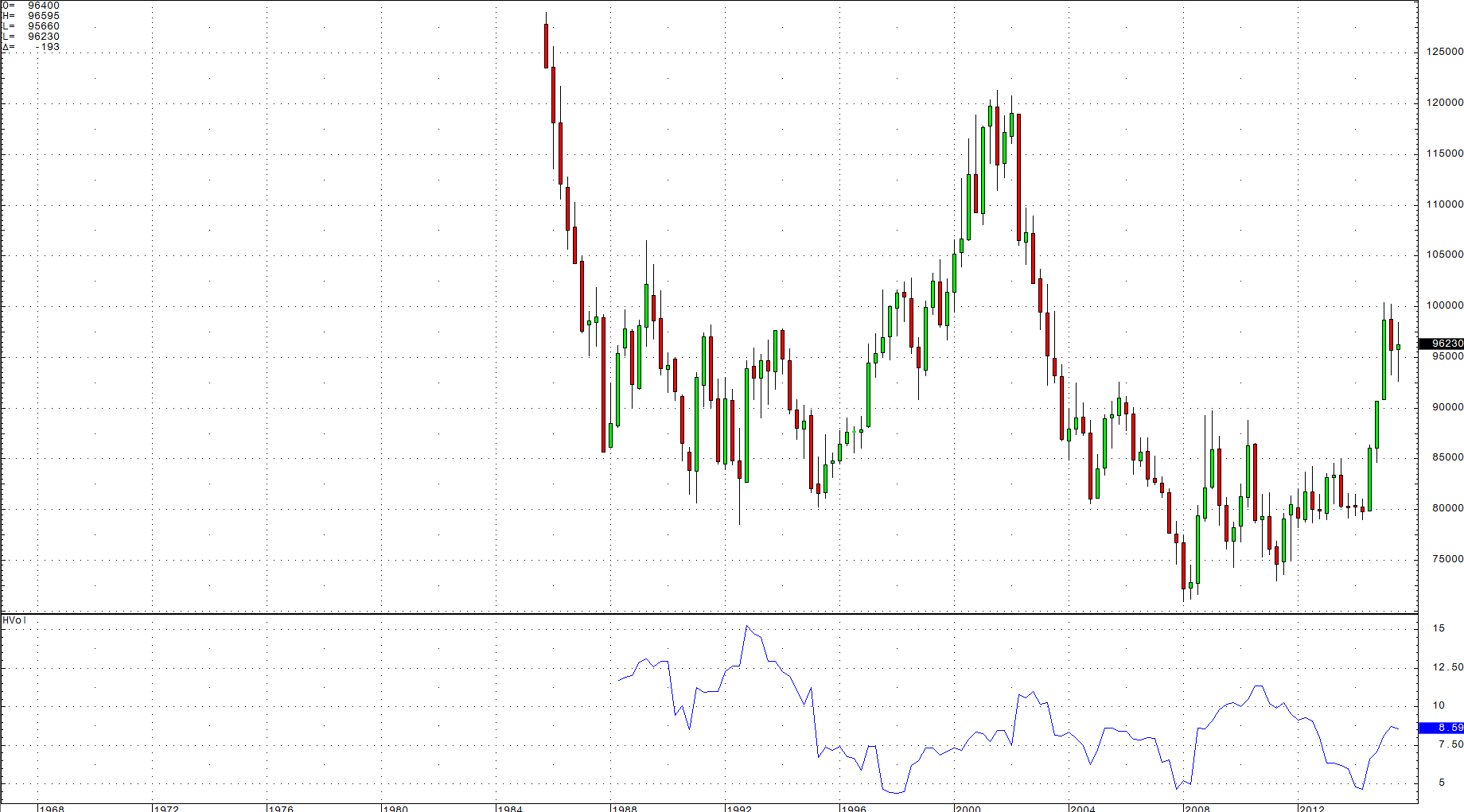

- Additionally, quarterly historical volatility for gold has increased to over 18%. I view this as an important factor for an analysis of the current price of gold. Commodities tend to trade at higher volatility than currencies. If gold were truly a currency, volatility would be lower.

(click to enlarge)

As an example, the quarterly historical volatility of the U.S. dollar index dating back to 1985 was never higher than 15.29% and currently stands at 8.59% – less than half the level of gold’s current quarterly historical volatility.

Gold was in a bull market prior to the global financial crisis of 2008. However, the rally only took it up to highs of $1,000 in pre-crisis trading. The true moon-shot for gold came as interest rates moved lower due to policies of quantitative easing to stimulate the U.S. economy in the wake of the 2008 crisis. That aggressive rally was likely a combination of fear and greed.

- Fear in that the crisis and QE resulted in doubts about the dollar and all fiat currencies as well as paper assets.

- Greed in that “paper gold” made a long position available to a huge new addressable market that would have never bought physical metal or traded futures.

Therefore, it is likely that the highs in 2011 resulted from a larger herd of buyers than during previous crisis periods. During that period, the fear and greed that drove gold considered the metal an alternative to the dollar or any other currency because of accommodative central bank policy to stimulate a faltering economy.

I believe the future price direction of gold can be determined if we can establish whether current market perception is changing and gold has reverted to commodity status.

If gold is a commodity, it is going to tank

The evidence is clear: commodity prices have been in a long-term bear market since 2011…[yet,] while gold has moved lower along with most raw material prices, it has remained much stronger than most.

- The price of copper is half what it was in 2011; if gold had a similar move, it would be trading at $960 per ounce.

- The current price of silver and platinum imply a gold price of $800 per ounce based on mean levels in their historical price relationships.

- Additionally, a reversion to mean in terms of the price relationship between corn, soybeans, wheat, sugar, crude oil and gold all yield the same results – a lower gold price.

If gold is a commodity, then the price is going much lower. A number of other factors also support this. The long-term gold chart is clearly bearish as the downtrend since 2011 is firm. In fact, that chart looks as if gold is preparing to fall off the edge of a cliff.

Gold & Inflation

Gold is an inflation hedge. Given the economic landscape in Europe and China, [however] the world is battling deflation rather than inflation these days. In a deflationary environment, the value of everything, including gold, goes lower.

One of the things holding the U.S. Fed back when it comes to fulfilling their promise to raise interest rates for the first time in a decade this month is that inflation is well below the central banks’ 2% target. The bottom line – again – is that if gold is a commodity, it is going to tank.

Moreover, the new “paper gold” products could exacerbate a down move as market participants hop on board a downtrend if the price begins breaking lower. Leveraged bearish ETF products could add insult to injury on the downside if gold moves into triple-digit territory. Remember, all commodities tend to take the stairs up and the elevator down. We saw a preview of that kind of action that back in July when gold dropped $50 on a 2.5 million ounce sell order on the opening of the Asian markets on a Sunday night in the U.S.

If gold is a currency, it could rally

If gold is truly a currency, it could rally in a flight to quality stoked by fear. However, I was disappointed in the action in gold when fear gripped markets on Monday, August 24. The Dow Jones Industrial Average traded down 1100 points in the opening minutes of trading. Gold only managed to rally to just under $1170 and as volatility in markets continued throughout the rest of the week, the price of the yellow metal dropped.

Furthermore, last week Mario Draghi, the President of the ECB, announced a more aggressive QE policy in Europe to stimulate the economy because data is showing that Europe is weaker than original expectations. He lowered estimates for growth out to 2017. It is likely that European interest rates, already at historical lows, will stay low for quite some time. Gold did not move higher on this news, which is a telling sign for now. The quandary for gold is that although lower interest rates are bullish, the European move is bearish for the euro and bullish for the U.S. currency.

Schizophrenia reigns supreme in the yellow metal

Gold is in a tough situation right now. It is an enigma and it is suffering from an identity crisis. It does not know whether it wants to be a commodity or a currency.

- Gold is expensive on a relative basis when compared to other commodities.

- Easy money policies around the world continue to debase the value of fiat currencies. The U.S. went through a long period of quantitative easing, which made money very cheap.

- Recently, the U.S. economy has shown signs of moderate growth and the Fed is likely to raise interest rates. This has contributed to a big rally in the dollar over the past year and that is not a positive for the price of gold.

- However, easy money is inflationary over the long haul. Europe’s QE policies, China’s devaluation of their currency and efforts to stimulate a slowing economy are causing those paper currencies to lose value as a side effect of stimulative policy. That should be positive for gold in the end, and it may be.

While I am bullish on gold in that I believe it is the ultimate store of value and, as such, we will see higher prices for the yellow metal in the future when the chickens come home to roost and the bill comes in for easy money policies, right now all evidence points to a continuation of the downtrend for gold.

Conclusion

I believe gold is acting more like a commodity than a currency these days, and we will likely see a price correction in the yellow metal. If gold decides it is a commodity, fasten your seatbelts – the ride down will be intense. My target on the downside is $880 per ounce. “Paper gold” product exuberance could make it uglier than that. The bottom line is that gold at $1122 is just too expensive.

*http://seekingalpha.com/article/3493776-the-modern-gold-market-an-enigma?ifp=0

Related Articles from the munKNEE Vault:

1. Gold – Is It A Commodity, A Currency, Neither or Both?

To answer the question “what drives the prices of gold” we have to determine the nature of gold. Is it a commodity, a currency, neither or both? This article does just that. Read on.

2. Gold Will Soon Revert To Bear Mode Trading On Way To $880/ozt.

If gold were to start moving appreciably higher it would damn all paper currencies…and given the current fragile state of the global economic landscape…governments around the world simply cannot, and will not, allow that to happen. They sit on big stocks of gold and, if necessary, they will use those reserves as a tool to crush rallies. I believe, therefore, that gold will soon revert to bear mode trading. My price target remains at the $880 level.

3. I See Gold Dipping To – Dare I Say – $880ozt. Here’s Why

Several signs have been flashing for the past year that gold has become too big for its britches and will eventually adjust to a lower price which could push the yellow metal off the edge of a cliff to – dare I say – not just below $1100 or $1000 per troy ounce, but to $880ozt.

4. The Gold Market: What Can We Expect In the Months Ahead?

We are at an interesting and perhaps critical juncture with respect to the direction of the gold price as it approaches a key support level. There are many mixed signals out there and the market seems to be vacillating, frustrating both bulls and the bears. Let us look at both cases in order to try to understand what the gold market may have in store for us during the coming weeks and months.

5. Analysts: Gold Will Bottom Somewhere Between $725 & $1,000/ozt.

Much has been written over the past few months as to just where gold (and silver) is headed. In light of the recent significant drop in price below is substantiation for such a decline and several projections as to where the price correction will bottom out and the timeframe for such price action.

6. New Update: Gold & Silver Will Plummet In 1st Qtr. of 2016 – Then Go Parabolic!

My new analyses of gold & silver indicates they will both continue to show weakness throughout the balance of 2015, plummet to $725ozt. & $12ozt. respectively, during the 1st. Qtr. of 2016 and then go absolutely parabolic in price by the end of 2016/early 2017. Below are the specific details of my forecasts (with charts) to help you reap substantial financial rewards should you wish to avail yourself of my insightful analyses.