Interest rates cannot stay low forever, however, so while the Fed’s low interest rate policy is pushing stock and bond prices higher, it is also infusing potential energy into the gold market. Therefore, it is only a matter of “When?” and not “If?” this trend reverses and gold catapults higher.

policy is pushing stock and bond prices higher, it is also infusing potential energy into the gold market. Therefore, it is only a matter of “When?” and not “If?” this trend reverses and gold catapults higher.

The above introductory comments are from an article* by Ben Kramer-Miller (GoldStockBull.com) entitled Gold Investors Shouldn’t Fear Rising Interest Rates: Here’s Why.

The following article is presented courtesy of Lorimer Wilson, editor of www.munKNEE.com (Your Key to Making Money!), and www.FinancialArticleSummariesToday.com (A site for sore eyes and inquisitive minds) and has been edited, abridged and/or reformatted (some sub-titles and bold/italics emphases) for the sake of clarity and brevity to ensure a fast and easy read. This paragraph must be included in any article re-posting to avoid copyright infringement.

Kramer-Miller goes on to say in further edited excerpts:

Investors commonly:

- assume that rising interest rates adversely impact the gold price, and vice versa,

- believe that a rising interest rate environment is indicative of a strong economy, which is supposed to drive investors out of gold and into the stock market and further

- assume that investors will want to exchange their gold, which has no yield, for stocks and bonds, both of which have yields and generate income

but this intuition is unfounded, at least when tracking the Fed Funds Rate since the Nixon abandoned the gold standard (i.e. after August 15th, 1971). Since then, a rising Fed Funds Rate has usually coincided with rising gold prices, and vice versa.

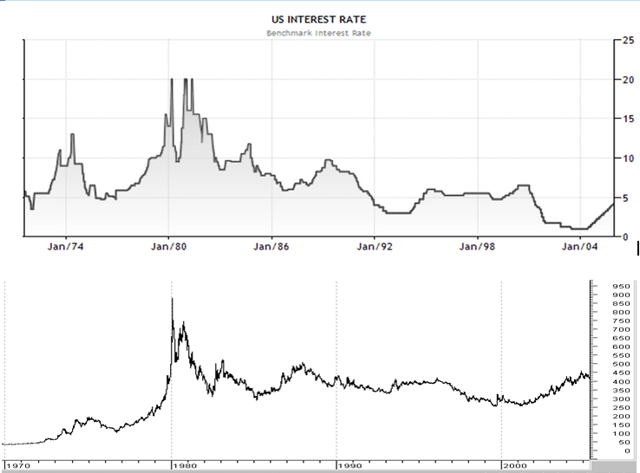

Consider the following data (gold price data is from Kitco, Fed Funds Rate data is from the St. Louis Fed):

- From August 1971 through December 1974 the gold price rose from $35 to $200 per ounce, while the effective Fed Funds Rate rose from 5.5% to 8.5%.

- From January 1975 through August 1976 the gold price dropped to just over $100/oz, while the Fed Funds Rate fell to 5.25%.

- In January of 1980 the gold price peaked at over $800/oz while the Fed Funds Rate rose to 14%.

- The gold price then fell to about $290/oz in late February, 1985, while the Fed Funds Rate fell to 8.6%.

- The pattern breaks here as the gold price rose to $500 in December, 1987 while the Fed Funds Rate continued to fall to 6.8%.

- However the trend continues as the gold price fell to $330 in March, 1993 while the Fed Funds Rate fell to 3%.

- The gold price then rose to $415 in February, 1996 while the Fed Funds Rate rose to 5.2%.

- The gold price then fell until hitting its September, 1999 bear market bottom at $255. This occurred just before the Washington Agreement on Gold was signed, while the Fed Funds Rate remained steady.

While the correlation is far from perfect, we can clearly see from the following charts that the Fed Funds Rate and the gold price move together more often than not and have similar trends over long time periods.

(Source: The Fed Funds Chart comes from TradingEconomics.com and the gold price chart comes from ChartsRUs.com)

What causes this strong correlation?

- When the Fed Funds Rate falls this creates a carry trade that allows banks to borrow cheap money from the Fed in order to buy assets with higher yields. It follows that bonds and stocks–or assets that have value insofar as they have a yield–become more attractive by comparison.

- More generally, when interest rates fall, the yield on interest-bearing assets becomes more attractive. A corollary of this is that assets that do not have any yield (i.e. gold and other commodities) become less attractive from an investment standpoint.

- Similarly, when the Fed Funds Rate rises this carry trade dissipates. Banks have to pay more in order to borrow, and so they are less willing to bid up the prices of income generating assets. As money comes out of these assets it finds a home in assets whose value is intrinsic.

In summary, a bank can make money if it borrows money from the Fed at 5% to buy an asset yielding 5.5% but if the Fed raises the Fed Funds Rate to 6%, that bank suddenly has to sell the asset yielding 5.5% or else it begins to lose money on the trade. Similarly, if the Fed Funds Rate drops to 4%, the bank has incentive to hold the asset even if it rises in value while its yield falls.

'Follow the munKNEE' daily! Here's why - Here's how

– Stop wasting time surfing the ‘net to find articles worth reading – we do it for YOU!

– We evaluate 100s of articles every day to find the most informative & well-written to share with you.

– The selected few are posted in an edited excerpts format with descriptive titles & introductory paragraphs to provide you with a fast & easy read.

– Avoid missing any articles by signing up here to have new posts sent to you automatically via our free Market Intelligence Report newsletter.

– munKNEE.com postings are also available on Twitter & Facebook. Check them out. You won’t be disappointed.

Ultimately we can conclude that:

- a high interest rate should indicate to investors that they should sell their gold,

- but a rising interest rate is a tailwind that will drive the gold price higher.

- a low interest rate is an indication that investors should buy gold,

- whereas a declining interest rate acts as a headwind.

It follows that the best time to buy gold is when rates are low, but set to move higher, and the best time to sell gold is when rates are high but set to move lower and, with the Fed Funds Rate at 0.1%, it is evident that gold is positioned to move substantially higher.

Editor’s Note: The author’s views and conclusions in the above article are unaltered and no personal comments have been included to maintain the integrity of the original post. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor.

After a long period of very low interest rates following the global financial crisis the central banks of the U.S. and U.K. are planning to gradually tighten their easy monetary policies as their economies improve. When their benchmark interest rates go up, interest rates elsewhere will go up to so should we worry if and when global financial conditions tighten? Read More »

2. We’re Doomed! Rising Interest Rates Will Cause Our Financial System To Implode

We’re doomed! Even if the economy were growing at a faster pace, it wouldn’t come close to offsetting the interest payments on our ever-expanding debt. As such, any sort of credit shock – either rising rates or a decline in the rate of debt expansion – will cause the system to implode. Let me explain why that is the case. Read More »