Everyone knows that interest rates are going to rise in the future so the real question is not whether they will rise, but when and by how much. [This article analyzes when that will most likely be.]

is not whether they will rise, but when and by how much. [This article analyzes when that will most likely be.]

The following article is presented courtesy of Lorimer Wilson, editor of www.munKNEE.com (Your Key to Making Money!), and www.FinancialArticleSummariesToday.com (A site for sore eyes and inquisitive minds) and has been edited, abridged and/or reformatted (some sub-titles and bold/italics emphases) for the sake of clarity and brevity to ensure a fast and easy read. This paragraph must be included in any article re-posting to avoid copyright infringement.

The Fed is expected to raise short-term rates in a very gradual fashion beginning next year, and five or so years from now rates are going to be topping out around 3½ to 4%.

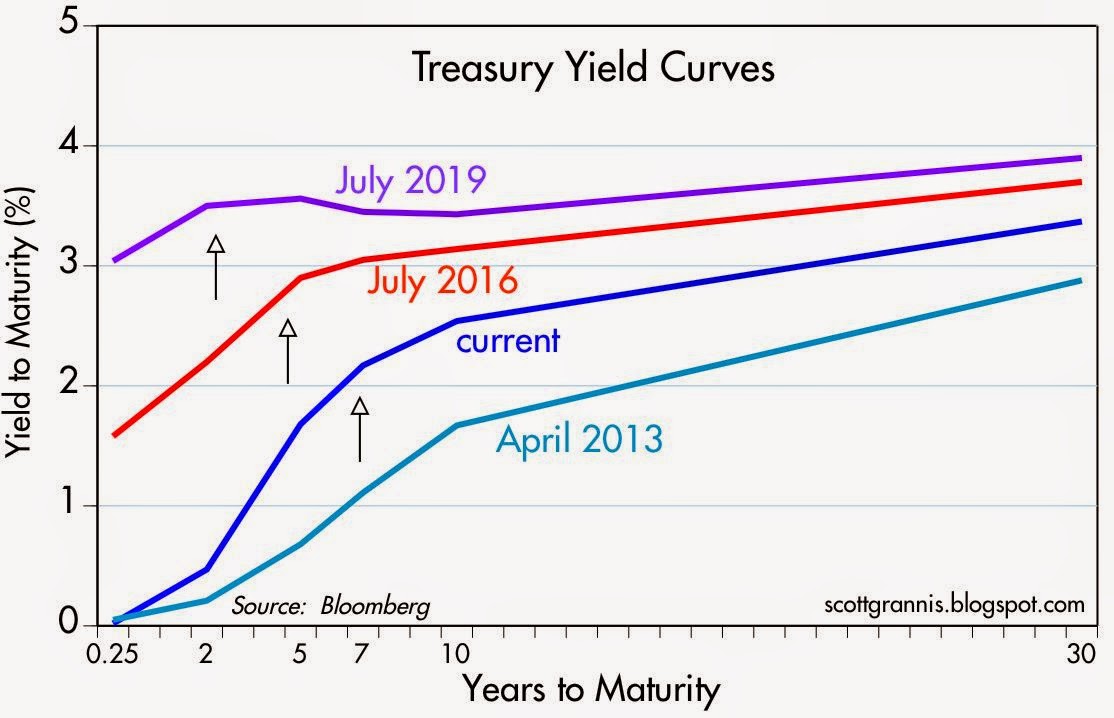

There’s nothing very scary about this. As the graph below shows, for most of modern history 5-yr Treasury yields have traded well in excess of 3%. That 5-yr yields today aren’t expect to rise above 4% for as far as the eye can see is pretty unusual from an historical perspective.

Interest rates aren’t expected to rise by much because:

- the market doesn’t think the U.S. economy has much chance of returning to its former growth glory, and

- the market doesn’t think that inflation has much chance of exceeding 2-3%.

In other words, the bond market today seems fairly convinced that growth will be sluggish and inflation will therefore be tame for as far as the eye can see.

- if you see more potential for growth and inflation, then bet that rates will rise faster than expected:

- lock in long-term borrowing costs today;

- keep the duration of bonds you own as short as possible; and

- avoid excessive leverage (or place hedges to protect against higher-than expected borrowing costs),

- consider an increased exposure to real estate, since it should benefit from stronger growth and higher inflation, and it is not necessarily expensive today and

- also consider an increased exposure to equities, since stronger growth and higher inflation should have a positive impact on future expected cash flows.

For my part, I acknowledge that I have been overly concerned about rising interest rates for most of the past 5 years or so. Being wrong for so long is humbling, but it is not a reason to shy away from worrying about a faster-than-expected rise in interest rates today. In the end, it’s all about what happens to the economy and to inflation.

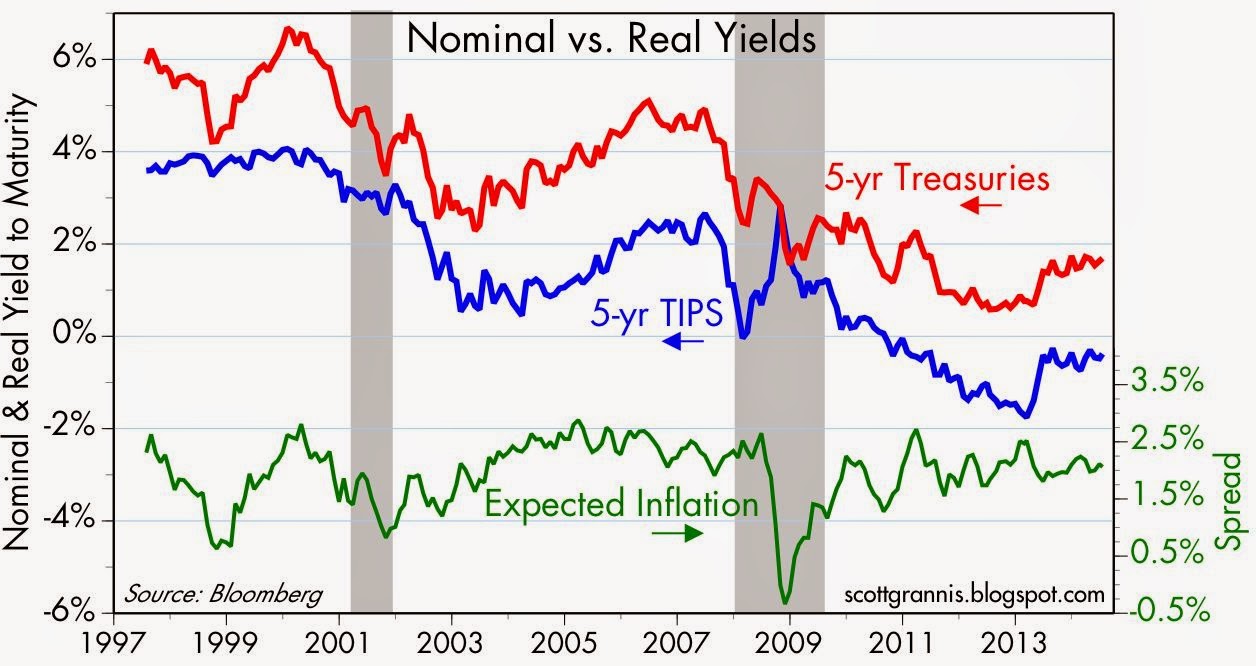

I’m still an optimist on the economy, since I think the market’s growth expectations are overly pessimistic. I think 5-yr real yields on TIPS tell us a lot about the market’s underlying expectations for real economic growth.

As the graph above suggests, the current -0.38% real yield on 5-yr TIPS points to economic growth expectations of perhaps 1% per year, which in turn is a bit less than we’ve seen in recent years. If the market were convinced that future growth would be a solid 3% a year, then real yields today would be a lot higher than they are now.

I’m still more worried about inflation than the market is, since I think the market is being a bit too complacent about the inflationary potential of the Fed’s massive balance sheet expansion and the Fed’s ability to reverse course in a timely fashion.

Editor’s Note: The author’s views and conclusions in the above article are unaltered and no personal comments have been included to maintain the integrity of the original post. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor.

Stay connected!

- Register for our Newsletter (sample here)

- Find us on Facebook

- Follow us on Twitter (#munknee)

- Subscribe via RSS

1. Political “Blame Game” Will Adversely Affect Your Portfolio – Here’s Why & How

The S&P 500 continues to hit new all time highs, but is your portfolio built on a house of cards? The politics to kick the proverbial can down the road may unleash dynamics that could be hazardous to your wealth. Here’s why and how to protect your portfolio. Read More »

2. Inflation or Deflation: Are We Approaching the Tipping Point?

Might our Inflation-Deflation Watch be suggesting a breakout in asset price inflation is about to take place? Could it, in fact, be presaging the start of John William’s hyper inflationary depression in which prices rise exponentially even in light of massive unemployment and bankruptcies? This article analyzes the situation. Read More »

3. Tips from TIPS on Prospects for Growth, Outlook for Inflation & Future for Gold

TIPS are telling us that the market is quite pessimistic about the prospects for real growth, but not concerned at all about the outlook for inflation. Read More »

4. Interest Rates NOT Rising Any Time Soon – Even With Fed Tapering. Here’s Why

Everyone and their mom is expecting long-term interest rates to rise now that the Fed is tapering its bond buying programs. I have a couple of problems with this line of thinking because, although it seems like reducing demand for a security (i.e. tapering QE) would result in a drop in price, when you really think about how quantitative easing works this makes no sense and, secondly, the market is telling us this makes no sense. Let me explain. Read More »