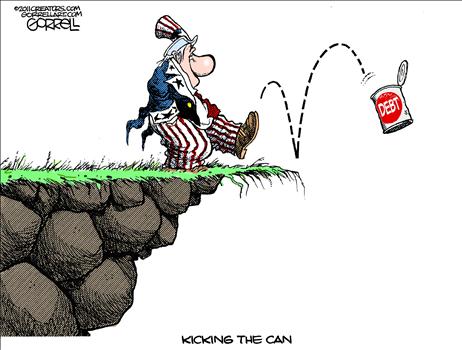

The S&P 500 continues to hit new all time highs, but is your portfolio built on a house of cards? The politics to kick the proverbial can down the road may unleash dynamics that could be hazardous to your wealth. Here’s why and how to protect your portfolio.

of cards? The politics to kick the proverbial can down the road may unleash dynamics that could be hazardous to your wealth. Here’s why and how to protect your portfolio.

The above introductory comments are edited excerpts from an article* by Axel Merk (merkinvestments.com) entitled Is Your Portfolio a House of Cards?

The following article is presented courtesy of Lorimer Wilson, editor of www.munKNEE.com (Your Key to Making Money!), and www.FinancialArticleSummariesToday.com (A site for sore eyes and inquisitive minds) and has been edited, abridged and/or reformatted (some sub-titles and bold/italics emphases) for the sake of clarity and brevity to ensure a fast and easy read. This paragraph must be included in any article re-posting to avoid copyright infringement.

Merk goes on to say in further edited excerpts:

The one thing politicians throughout the world have in common is that they rarely ever blame themselves. They tend to diffuse responsibility or place blame on groups such as political opponents, the wealthy, or foreigners.

If you now add that we have very real and major challenges in the world, it may be reasonable to assume that policy makers will continue to remain engaged in “fixing” things by blaming others. As an investor, if nothing else, this means asset prices may continue to move away from fundamentals and reflect the next perceived intervention by policy makers. This presents challenges for investors trying to maintain the real purchasing power of their portfolio and avoid a major drawdown at the wrong time.

One of the most relevant dynamics for investors to be aware of is that the interests of a government in debt are not aligned with the interests of investors. A government in debt has an incentive to debase the value of its debt, whereas investors have an interest in earning a positive real return on their savings.

I attended a conference at Stanford’s Hoover Institution recently where academics, as well as four acting Fed Presidents, pondered about the future of central banking. One of the presenters, Stanford Professor Dr. Martin Schneider, had some blunt words that were as obvious as they were controversial: monetary policy cannot be conducted in a vacuum, and is very much dependent on fiscal policy. He pointed out that as interest rates rise, taxes would have to go up to pay for the higher cost of servicing the debt.

Dr. Schneider presented a simplified model of the world, arguing that in the U.S., in today’s environment, both government and citizens would benefit from inflation – the losers would be foreigners. While anyone can take issue with a simplified model; and I could also argue why everyone loses with inflation, such details should not distract from the message, though, and that message was that:

- Inflation debases the value of government debt

- Inflation debases the value of consumer debt

- If you are a consumer with savings, sorry, you are in the minority and your interests will have to take a back seat

- Given that foreigners hold large amounts of Treasuries, they are on the losing end in an inflationary environment

We can argue whether inflation is a problem today or whether it is not but it’s difficult for me to argue with the above.

The conclusions I draw are:

- Political stability throughout the world will continue to decline

- Traditional diversification can’t be relied upon as asset prices reflect the next perceived move of policy makers rather than fundamentals

- Asset bubbles will be fostered

- Bonds are vulnerable

- The U.S. dollar is vulnerable

- Investors may need a toolbox to counter the toolbox of policy makers

The investment tools we have been focusing on to tackle these challenges at the core are currencies and gold.

- Gold may do well as the value of debt (and with it the dollar) is debased;

- gold also has historically had a low correlation to other asset classes, thus serving as a candidate diversifier going forward.

- Currencies can also serve as valuable tools: with currencies, one can design a portfolio that has a low correlation to other asset classes;

- currencies are historically less volatile than gold. On the other hand, other countries also face challenges, so some thought has to be put into a currency driven strategy.

We can’t know for certain that either currencies or gold will protect investors against a collapse of the proverbial house of cards, but we are afraid that ignoring these dynamics could be perilous.

Editor’s Note: The author’s views and conclusions in the above article are unaltered and no personal comments have been included to maintain the integrity of the original post. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor.

*http://www.merkinvestments.com/insights/2014/2014-06-05.php (© 2014 Merk Investments LLC)

Stay connected!

- Register for our Newsletter (sample here)

- Find us on Facebook

- Follow us on Twitter (#munknee)

- Subscribe via RSS

Related Articles:

1. Monetary System Collapse Guaranteed – Here’s Why & How to Invest & Insure Your Wealth Accordingly

Our monetary system is guaranteed to collapse. The central banks prints money like there is no tomorrow. The governments spends like a drunken sailor and yet inflation is benign and interest rates sit at generational lows. Banks are gaining in profitability while their bad debts are being erased by rising asset prices. What’s not to like? Plenty! This article goes into the details of the money creation process to understand how and why this is happening, what the future implications will be and how to best invest to protect oneself from these eventualities. Read More »

2. Gold Going Parabolic In Next Few Years – Here’s Why

We are now starting the hyperinflationary phase in the USA and many other countries as a result of the accelerated fall of the U.S. dollar and this will be reflected in the parabolic rise in the price of gold over the next few years. Read More »

3. Probability of Deflation Is 60%, Inflation Is 25% and Muddling Through Is 15% – Here’s Why

At the end of last year virtually every every single economist expected interest rates to rise this year as the Fed tapered their purchases and the economy improved but, in fact, interest rates on the 10 year U.S. Treasury have been going down year to date (from 3% to 2.5% after rising from about 1.6% to 3% last year). The masses, going along with this crowd, got fooled but we have been calling for a decline in interest rates for some time now due to world-wide deflation and it couldn’t be clearer to us that this is the most likely scenario for the United States. Let us explain. Read More »

4. A Crash of the Financial & Monetary System Seems Inevitable. Here’s Why & How to Prepare

A crash of the financial and monetary system seems inevitable. This presentation connects the dots between issues like currency wars, rigged markets, central bankers’ interventions, statistics manipulation, monetary mismanagement and financial repression in a factual way that is also easy to understand. Read More »

5. Physical Gold Cannot Possibly Lose Out Over Fiat & Digital Currencies – Here’s Why

Gold cannot possibly lose its central position as the pre-eminent money used by the world for thousands of years. The aggressive measures of the Anglo-American Axis with regard to gold are absurd and they will lead to total disaster both for the Axis, and for the world which has been forced to follow its lead for over forty years. Read More »

6. Own Any Foreign Currencies? Perhaps You Should. Here’s Why

Obtaining a second passport and an offshore bank account are crucial parts of an overall diversification strategy, but they are not the only ones. Capturing international opportunities for your investment portfolio also has an important role and one of the easiest ways to do this is to own foreign currencies. Below are my 10 favorite reasons for doing so. Read More »