…The more I think about where the “monetary policy community” of academic elites has brought us, the angrier I get. It has been a long time since I have been this passionately upset about something – and not merely because the policies are stupid – but what the Fed has done is to destroy the retirement hopes and dreams of multiple tens of millions of my fellow U.S. boomers (and when we include the effects of the destructive policies of the rest of the world’s central banks, the number becomes hundreds of millions). This article looks at the FOMC’s decision-making process for monetary policy and surveys the unpalatable future that our leaders are cooking up for us.

the angrier I get. It has been a long time since I have been this passionately upset about something – and not merely because the policies are stupid – but what the Fed has done is to destroy the retirement hopes and dreams of multiple tens of millions of my fellow U.S. boomers (and when we include the effects of the destructive policies of the rest of the world’s central banks, the number becomes hundreds of millions). This article looks at the FOMC’s decision-making process for monetary policy and surveys the unpalatable future that our leaders are cooking up for us.

The comments above and below are excerpts from an article by John Mauldin (MauldinEconomics.com) which may have been enhanced – edited ([ ]) and abridged (…) – by munKNEE.com (Your Key to Making Money!)

to provide you with a faster & easier read. Register to receive our bi-weekly Market Intelligence Report newsletter (see sample here , sign up in top right hand corner.)

The secure and protected world our central bankers live in is far removed from that of the American or European middle class retiree. The purity of their theory and the clarity of their economic thought is evidently far more important to them than people’s wellbeing is…Central bankers of the world look around them and see nothing but confirmation of their brilliance. Mostly they see it reflected from the stock markets, but some of us are beginning to think they are going blind.

Almost everything the Fed did to us since 2008 falls into two broad categories: interest rate repression and quantitative easing.

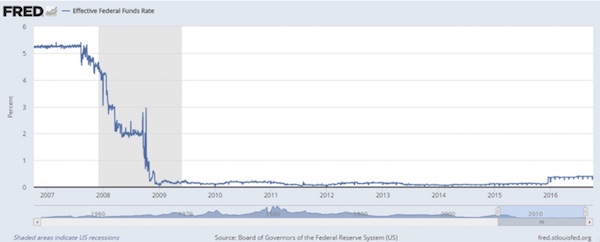

Here is the federal funds rate from 2007 to 2016. The shaded area is what we now call the Great Recession.

The Federal Open Market Committee entered 2007 with the rate target at 5.25%. They starting lowering it in August of that year – months before the economy went into recession. Why was that? Recession or not, many folks weren’t doing well. Even then there was talk of banks having difficulty, though the worst was yet to come.

Look how fast rates fell. In July 2007 savers could buy Treasury bills, certificates of deposit, or other principal-protected savings instruments and enjoy a 5% or better risk-free yield. Longer-term fixed-income products actually offered even higher yields. A year and a half later, the fed funds rate was bumping the zero bound, and savers could make nothing without taking on market risk, which few wanted to do at the time, because iconic brands were blowing up everywhere.

Here is the great irony and possibly the most iniquitous part of the Fed’s monetary policy initiative. They wanted investors to move out on the risk curve – but did they bother to look at the demographics of this country? We have a huge bulge of Boomers – retirees and near-retirees who do not need to be moving out the risk curve at this time in their lives – who need Steady-Eddie returns, and they need to be reducing their risk, not increasing it.

A sober look at the current economic environment reveals overvalued, overbought, and illiquid markets everywhere. The global central bank community’s ultra-low and negative interest rates have created an environment of risk that is looking more and more like a bubble in search of a pin. If and when it bursts, it will take the retirement dreams of millions of Americans with it.

From the Fed’s perspective, super-low interest rates were economic stimulus. With borrowing costs so low, we were all supposed to race out and buy stuff. Companies should have expanded and hired more workers. Homebuilders should have been incentivized to build more McMansions in the suburbs, knowing qualified buyers would appear like magic. What was supposed to happen was a normal recovery. What we got was the weakest recovery on record…[What] we got [was] stimulus for Wall Street in the form of QE, and it led to an inflation of asset prices. No one really minds if the value of their stocks, real estate, and other assets go up; and there was the assumption that a rise in the stock market and real estate would trickle down to Main Street. Clearly, it has not…

What did happen was the opposite of stimulus, at least for those who were not the direct beneficiaries of quantitative easing…i.e. the people who actually wanted to be prudent and save and put money in fixed-income and certificates of deposits. Remember when you could invest in a CD at 5% to 6%? What a quaint notion.

By reducing the incomes of retirees and terrifying near-retirees, the Fed successfully reduced economic activity. Hopefully, that was not their intent, but that is what happened. They claim they managed to save the banking system from collapse, and I would agree that QE1 was necessary and beneficial to the system. I guess that’s something to their credit, but it came at tremendous cost. They put much of the cost of rescuing the banks on the shoulders of completely innocent people. The cost was borne by savers and small investors…

I believe we are again suffering the effects of a massive monetary policy error. The error has already been committed, but we have just begun to endure the consequences. We are still living in a dream, but we’re nervous, much like we were in 2006. The Federal Reserve has repeated the mistakes of the last cycle. They have kept rates too low for too long, but this time they have outdone themselves, clinging desperately to the zero bound. In doing so they have financialized the economy and made it hypersensitive to interest rate moves…

Low interest rates have traumatized US pension funds and basically made it impossible for funds to meet their investment targets – and the consultants to whom the funds pay large fees are still showing them models (based on gods know what assumptions) that say it is okay to project 7% to 7.5% compound returns for the future.

So here we are, in a weak recovery that grows longer in the tooth with each passing month. I have discussed the assorted potential crises that could set off the next recession. You know the list: China, Japan, Italy, Germany (99% of investors do not understand how vulnerable Germany is), our own elections here in the U.S., or just a gradual slowdown as consumers lose the will or ability to spend. Something will happen to set off another shock, and it will probably happen in the next year or two. Then what?

Conclusions

This brings us to perhaps the biggest danger of all…most Americans are skeptical of the Fed’s happy talk and no longer believe that Fed policies will result in the economic growth projected. Sadly, that group of “most Americans” does not include Federal Reserve governors and bank presidents. All evidence suggests they believe their policies are working out swell. Unemployment is down, so Janet Yellen is happy. Stocks are up, so Stanley Fischer is happy. They invited all their friends to Jackson Hole to plan the next party, in which they will spin the bottle on negative rates and try to get Congress to eliminate $100 bills. They think it will be fun. Many in the economics profession want to party with them.

We will have another financial crisis and/or recession, probably soon, and we can’t trust the Fed to respond correctly. We’ll be lucky if whatever comes out of their Frankenstein lab is only ineffective. There’s a very real risk they will make the situation far worse. The masses of unprotected people are in no mood to swallow more monetary policy medicine, much less any additional remedies that globalist plutocrats may try to shove down their throats…

Winter is coming. You need to have a plan. Over the next few months I will be talking about how I intend to get through the coming economic winter. If my plan does not work for you, then you need to come up with your own. Hope is not a strategy, my fellow Baby Boomers.

Follow the munKNEE – Your Key to Making Money!

- “Like” this article on Facebook

- Have your say on Twitter

- Register to receive our bi-weekly Market Intelligence Report newsletter (see sample here , sign up in top right hand corner)

- Share your thoughts with us in the comments section below. We’d like to hear from you!