If Congress addresses the issue by maintaining the current tax and spending policies we will get more of the same economy we have experienced for the past three years, all else being equal. [That being said,] what if Congress goes over the fiscal cliff hit? This blog post is designed to assess the impact. Words: 1362

So says Ron Rimkus, CFA in edited excerpts from a guest post* on http://blogs.cfainstitute.org entitled The US Fiscal Cliff: Assessing the Impact.

Lorimer Wilson, editor of www.munKNEE.com (Your Key to Making Money!), may have edited the article below to some degree for length and clarity – see Editor’s Note at the bottom of the page for details. This paragraph must be included in any article re-posting to avoid copyright infringement.

Rimkus goes on to say, in part:

To grapple with the possible impact of the fiscal cliff we must answer the following questions:

What is the likelihood that U.S. Congress will address the fiscal cliff before it goes into effect?

How bad is the current fiscal deficit situation in the United States?

What has been the impact of austerity programs historically?

Is there anything terribly unique about the situation in which the United States finds itself?

…To put the fiscal deficit into proper perspective, consider the history of U.S. fiscal surpluses (or deficits) as a percentage of GDP since 1947.

First, note how the United States immediately drifted from regular fiscal surpluses to fiscal deficit after it exited the gold-exchange standard in 1971.

Second, the United States is clearly in uncharted waters at present, with the average fiscal deficits since the 2008 financial crisis amounting to about −8.3% of GDP.

United States: Fiscal Surplus (Deficit) as a Percentage of GDP

(click to enlarge)(Click to enlarge)

Sources: BEA, CFA Institute.

It is believed by many — including the Congressional Budget Office — that the Budget Control Act will cut the deficit nearly in half, to approximately −4.2% of GDP. The questions that the markets are wrestling with now are:

what impact the reductions in government spending will have on the U.S. economy and

what impact the sharp escalation of taxes may have.

The above changes are happening simultaneously, however, so it is instructive to separate them for the purpose of analysis.

Who in the world is currently reading this article along with you? Click here

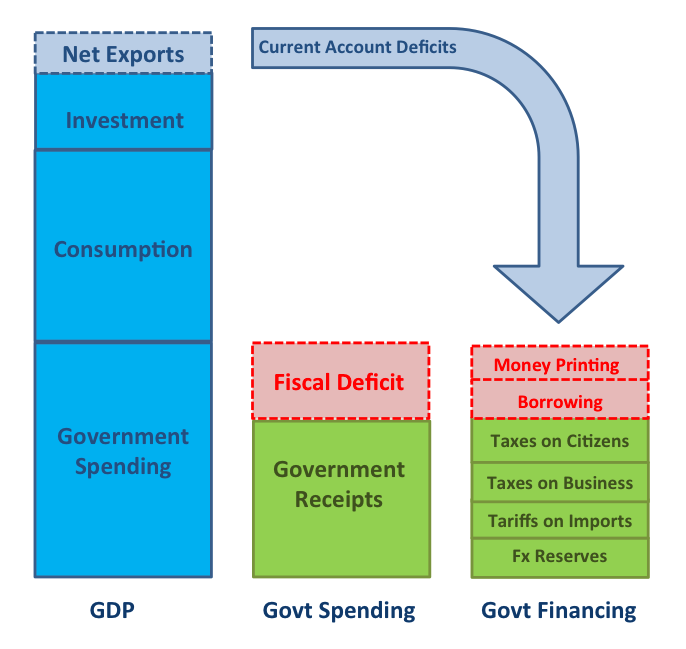

Now consider the equation for GDP: GDP = Consumption + Investment + Government spending + (Exports − Imports). This equation cannot be viewed in isolation however.

The GDP equation includes government spending, and it is easy to fall prey to the simplistic notion that more government spending translates into more GDP. [However,] because government spending is a function of many things, including the ability of the government to finance itself, it can have a direct impact on the other variables in the GDP equation.

Governments, as illustrated in the following graph, finance themselves through some combination of:

direct taxation of citizens,

taxation of businesses,

tariffs on imports from other countries,

buildup and usage of foreign currency reserves from international trade,

issuance of debt, and

money printing.

(click to enlarge)(Click to enlarge)

Changes in each of [the above] components of government finance can impact:

consumption and investment as well as

exports and imports (not to mention exchange rates)

[therefore],

as government spending rises, it may cause spending on consumption, investment, and/or net exports to fall and monetary and fiscal policies designed to offset any negative effects of stimulus have numerous trade-offs themselves. For example, the Fed’s explosion in the monetary base has caused a substantial increase in the prices of many commodities relative to other goods, slowing both consumption and investment from what they otherwise would be

as marginal tax rates come down, does aggregate tax revenue to the government fall — or rise? Recent work by Thomas Sowell of the Hoover Institution highlights numerous historical examples in which decreases in marginal tax rates have increased aggregate tax revenues to the government by material amounts. It is clear in many historical situations that high tax rates have encouraged both legal (and perhaps illegal) tax evasion as well as discouraged productive investment of capital. These are important concerns because the sensitivity to tax rates directly affects the amount of investment and consumption that take place within the GDP equation.

Considering all the above interrelationships among the variables of GDP, it is not possible to create a general rule as to what might happen without more information.

Government activity can be productive in some areas and counterproductive in others – so which areas are getting cut?

How productive or counterproductive is a particular government on average? Comparable tax hikes in the United States and Uganda might have radically different effects on the economy.

The question, as always, is whether the specific programs or projects are productive uses of capital so talking in broad brush strokes is useless.

It contains the “best of the best” financial, economic and investment articles to be found on the internet

It’s presented in an “edited excerpts” format to provide brevity & clarity of content to ensure a fast & easy read

Don’t waste time searching for articles worth reading. We do it for you and bring them to you each day!

Sign up HERE and begin receiving your newsletter starting tomorrow

What is perhaps most troubling about all the discussions of how GDP responds to government spending is the absence of a discussion of the debt the government borrows to achieve GDP growth.

Combined with easy-money policies from the U.S. Federal Reserve, the private sector splurges on debt too. Aggregate credit outstanding in the United States is $56 trillion compared to a U.S. economy (i.e., GDP) of $15 trillion — and aggregate credit is growing at about 5%, while GDP is growing at about 2%. [As such,…] the absolute increases in debt are greater than the corresponding absolute growth in GDP so where is that incremental money going? Are companies taking out reams of new debt only to place it in cash on their balance sheets (it seems unlikely)…or is it a reflection of the inefficiency of government spending today?

The fiscal cliff issue raises some very fundamental [tenants] about the role, the capabilities, and the limitations of government, namely that:

Government should spend money on things where the private sector cannot organize and perform efficiently on its own (e.g., establishing a common defense, building an interstate highway system, or creating rules for laying utility lines or fiber optic cable, etc.)

Government should invest in projects in which the government can employ that capital more effectively than the private market….

The above become the benchmark for judging existing government spending and whether or not increases or reductions in government spending are good or bad. The Budget Control Act makes cuts across the board, so the question becomes how productive or unproductive is government spending right now.

Recently, the International Monetary Fund came out with an analysis which suggests that the multiplier on government spending is greater than previously believed. The old rule of thumb for the multiplier was that it is about 0.5 (depending on your source). Their new estimate is somewhere between 0.9 and 1.7 meaning that $1 billion in incremental government spending translates into somewhere between $900 million and $1.7 billion of GDP growth. This analysis, however, does not address the accumulation of debt and whether or not the additional debt is creating larger and larger problems to be faced in the future…so it seems that the exclusive focus on GDP is misplaced….

*http://blogs.cfainstitute.org/investor/2012/11/12/us-fiscal-cliff-gauging-the-observer-effect/ (Disclaimer: Please note that the content of this site should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute.)

Editor’s Note: The above post may have been edited ([ ]), abridged (…), and reformatted (including the title, some sub-titles and bold/italics emphases) for the sake of clarity and brevity to ensure a fast and easy read. The article’s views and conclusions are unaltered and no personal comments have been included to maintain the integrity of the original article.

It’s easy to find analysts and investors who are certain that a deal [to avoid the fiscal cliff] will be reached, or at least that the can will be kicked down the road to buy more time. It’s also easy to find more pessimistic views that are based on the lack of cooperation in the past, and a deeply polarized country and political system. However, I think many are missing the point, which is that austerity is coming to America – taxes are going up and government spending will be reduced – [and. as such,] the United States is likely to face a recession and market correction in 2013, regardless of whether or not a compromise is reached over the Fiscal Cliff. Words: 970

What is the “Fiscal Cliff”? What would its ramifications be? Will it tip the U.S. into a recession? What are the critical economic building blocks that would be adversely affected? How best should you position your portfolio for such an eventuality.

We all know that high debt is a growth killer and, at the moment, the U.S. has a budget deficit of about $1 trillion. That’s a very big number…The question is, at what point do countries have to deal with high debt levels? How high do debt levels have to be before one has to deal with the problem by lowering budget deficits? Also, what are the consequences of such debt and budget reductions? Words: 500

“Portfolio managers have been swayed by hope over experience” when it comes to anticipating the effects the fiscal cliff will have on markets. Investors aren’t giving as much attention to the fiscal cliff as they should be, and that may be helping to set the markets up for a repeat of last year, when the debt ceiling negotiations sent stocks plummeting.

The outcome of the election of 2012 will [only] determine the rate of speed at which we approach the [financial] cliff [because] neither political alternative is willing to change course, to steer away from the cliff. The cliff is so high that whether we go over it at 200 mph (Obama) or whether we merely slip over the edge (Romney), the end result is the same — fatal for the economy and perhaps our entire political system. It is the fall that will kill us. [This article explains why that is going to be the case.] Words: 1135

Under current law, a sharp reduction in the federal budget deficit between 2012 and 2013 will cause the economy to contract but, the Congressional Budget Off ice projects, will also put federal debt on a path more likely to be sustainable over time. To illustrate the eff ects of fiscal tightening, CBO compared its projections under current law (the “baseline” projections) with projections under an alternative set of policies — two scenarios in a broad spectrum of choices – in the infographic below.

The U.S. federal government is scheduled to implement a fiscal tightening of unprecedented severity (approx. 5% of GDP) at the start of 2013. The last time a tightening of such proportions occurred (3% of GDP in 1969) it presaged a recession. Thus, unless mitigated by an act of Congress, we expect the fiscal cliff would lead the U.S. into a recession in 2013. Below, in 26 charts, we examine all aspects of the impending crisis to gauge its potential impact on the credit markets and, by extension, our strategic investment recommendations.

This post shows JPMorgan’s estimated probabilities on four different fiscal cliff outcomes, conditional on who wins the presidential election in November.

Unless the government acts quickly, it is probable that the term “fiscal cliff” will become a household phrase over the next few months. Unfortunately, this is reminiscent of the budget ceiling crisis about a year ago. In this report we will explain what the cliff is, discuss the worst case scenario, and determine what, if anything, you should do about it. Words: 1436

The International Monetary Fund, the U.S. Congressional Budget Office, the National Association of Manufacturers and many other authorities are now warning that with the largest tax increase in U.S. history — plus the largest government spending cuts our nation has ever seen – one of the deadliest financial crises in U.S. history is set to strike the U.S. economy beginning this coming New Year’s Day. Barring a miracle in Washington….. Words: 1028

policies we will get more of the same economy we have experienced for the past three years, all else being equal. [That being said,] what if Congress goes over the fiscal cliff hit? This blog post is designed to assess the impact. Words: 1362

policies we will get more of the same economy we have experienced for the past three years, all else being equal. [That being said,] what if Congress goes over the fiscal cliff hit? This blog post is designed to assess the impact. Words: 1362 (Click to enlarge)

(Click to enlarge) (Click to enlarge)

(Click to enlarge)