If you thought the Eurozone crisis was in the past, think again…It’s a near  mathematical impossibility that its weakest members can grow their way out of their debt and if deflation takes hold—as it has already in Greece and Cyprus, and is close in Portugal, Spain, and Italy—all bets are off.

mathematical impossibility that its weakest members can grow their way out of their debt and if deflation takes hold—as it has already in Greece and Cyprus, and is close in Portugal, Spain, and Italy—all bets are off.

The above introductory comments are edited excerpts from an article* by Martin Fluck (www.caseyresearch.com) entitled The Stress Tests That Could Stress Markets.

The following article is presented courtesy of Lorimer Wilson, editor of www.munKNEE.com (Your Key to Making Money!), and www.FinancialArticleSummariesToday.com (A site for sore eyes and inquisitive minds) and has been edited, abridged and/or reformatted (some sub-titles and bold/italics emphases) for the sake of clarity and brevity to ensure a fast and easy read. This paragraph must be included in any article re-posting to avoid copyright infringement.

Fluck goes on to say in further edited excerpts:

Europe’s financial markets remain jittery because its…banks still haven’t repaired their balance sheets, so they’re not willing to lend to each other – never mind lending to small and medium-sized businesses – and, given that the Eurozone ’recovery’ is losing momentum...everyone is terrified that it could well end up in a deflationary debt spiral. Right now, the omens aren’t good.

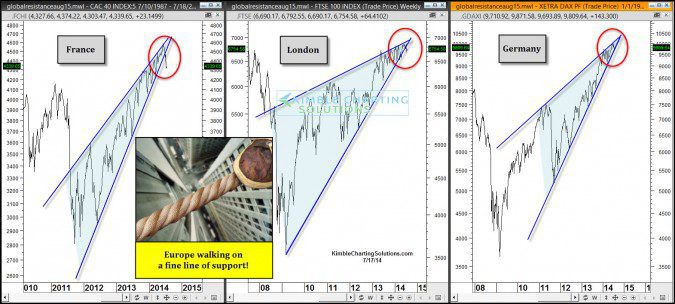

[Indeed, according blog.kimblechartingsolutions.com** “the strong rallies in London, Germany & France over the past few years have created steep bearish rising wedges, which two-thirds of the time result in lower prices. While the trend is up in all three of these key markets each is walking on a fine line of support. A break of support here could set off a wave of selling pressure.“]

The ECB’s monetary stimulus is not being transmitted to the countries where it’s most needed. The Spanish and Italian corporate sectors, dominated by smaller firms that are dependent on banks for finance, must pay much higher borrowing costs than small firms in northern Europe. In May, household loans in Europe declined at the fastest rate ever recorded—and the largest decline in lending to non-financial corporations occurred in Italy and Spain.

Since ECB president Mario Draghi said he’d do “whatever it takes” to save the euro in 2012, real inflation-adjusted lending rates for nonfinancial businesses have actually risen steadily. In Spain, rates are back up to their 2009 peak:

The Eurozone remains unstable, because its monetary system is flawed.

- The euro allows stronger countries like Germany to benefit from lower borrowing costs, capital inflows, and the immigration of skilled workers.

- Meanwhile, higher real interest rates in weaker countries push them ever deeper into deflation.

Unless the Eurozone is prepared to become a United States of Europe and raise taxes at a European level, Europe will never experience an economic convergence. We know, however, that Europe’s politicians are never going to give up their national sovereignty to create a genuine fiscal, political, and monetary union. They couldn’t even agree to share risk across national lines by forming a proper banking union.

As growth slows, the ECB is getting desperate.

- It lowered its benchmark interest rate to 0.15% and

- introduced negative interest rates on bank deposits in June. Neither will make much of a difference.

…Quantitative easing would.t help either, even if the ECB could overcome Germany’s opposition to it. Businesses and consumers are already maxed out, and the ECB has already monetized banks’ excess collateral…

The euro crisis is now in its fifth year, and investors should brace for sovereign defaults. Perhaps Italy and Greece will force the issue. History shows that heavily indebted countries are most likely to default, once they have achieved primary budget surpluses—like Italy and Greece have. In the face of 26.7% unemployment and growing political extremism, the temptation to quit the euro must be growing.

The belief that the euro has been saved is lulling investors into taking on too much risk, as they did in 2007. Whatever the outcome of the EU’s stress tests, it’s only a matter of time before the Eurozone debt crisis re-erupts.

Editor’s Note: The author’s views and conclusions in the above article are unaltered and no personal comments have been included to maintain the integrity of the original post. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor.

*http://www.caseyresearch.com/cdd/the-stress-tests-that-could-stress-markets (© 2014 Casey Research, LLC; All rights reserved) **http://blog.kimblechartingsolutions.com/2014/07/europe-is-walking-a-very-fine-line-here-watch-the-next-step/#sthash.tPeqpsa6.yxSDpwAq.dpbs

Follow the munKNEE!

- Register for our Newsletter (sample here)

- Find us on Facebook

- Follow us on Twitter (#munknee)

- Subscribe via RSS

Related Articles:

1. Europe to Lurch From Frying Pan of Depression to Fire of High Inflation (& the U.S.?)

In the coming years, Europe appears set to lurch from the frying pan of depression to the fire of high inflation. When it does, the lessons of the Great Inflation [outlined in this article] will suddenly be all too pertinent. Read More »

2. It’s Time to Invest In Europe – Here’s Why & How

The Eurozone economy (and currency) – which was once on the brink of complete and utter disaster – is finally on the road to recovery….[Here is] a safe way for skittish investors (i.e. – the non-contrarians) to take advantage of the opportunity in Europe before it disappears. Words: 503; Charts: 1 Read More »

3. European Debt Problems Continue to Escalate

With stocks at record highs and the U.S. economy improving, the European debt crisis seems like a distant memory….[While] Europe is no longer the market’s focal point, however, that doesn’t mean the euro zone’s financial problems have gone away. Read More »

4. France is Eurozone’s Biggest Risk to Economic Recovery – Here’s Why

France continues to pose the biggest near-term risk to the euro area’s economic recovery. Why France some may ask? [Here’s why.] Read More »