…If you’re retired and withdrawing from your portfolio, the “sequence-of-return” risk…can upend your entire retirement. [Here’s why.]

This version of the original article, by John Coumarianos, has been edited* here by munKNEE.com for length (…) and clarity ([ ]) to provide a fast & easy read.

This version of the original article, by John Coumarianos, has been edited* here by munKNEE.com for length (…) and clarity ([ ]) to provide a fast & easy read.

The Math Is Different in Distribution

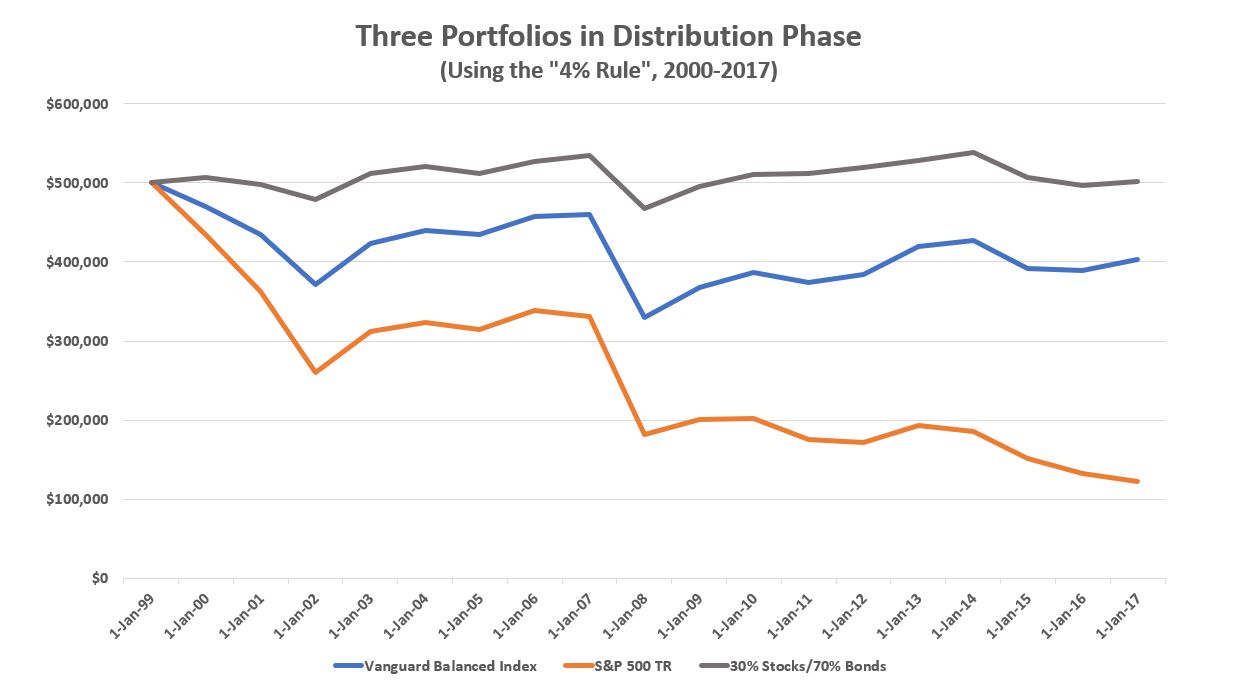

…The “sequence-of-return” risk – the problem of the early years of withdrawals coinciding with a declining portfolio – can upend your entire retirement… because a portfolio in distribution that experiences severe declines at the beginning of the distribution phase, cannot recover when the stock market finally rebounds. Because of the distributions, there is less money in the portfolio to benefit from stock gains when they eventually materialize again…

…Investors close to retirement should keep that in mind because current stock prices are historically high and bond yields are historically low. That means the prospects for big investment returns over the next decade are dim and that increasing stock exposure could be detrimental to retirement plans once again.

In my example below, decreasing stock exposure benefits the portfolio in distribution phase, and that could be the case for retirees now.

The Psychology Is Different In Distribution

…It isn’t just that stock prices are high and that bond yields are low now, [however]…because your mindset is likely different too; Your retirement is closer at hand and starting to seem like a realistic possibility. It’s not fun to see your portfolio drop from $500,000 to $225,000 when you’re 45 but it’s way worse to see your $1 million portfolio drop to $450,000 when you’re 55 and beginning to think serious thoughts about the when and how of your retirement. The losses are the same (in percentage terms); the ages are different. In other words, your proximity to retirement could make you sell at the bottom more than it might have a decade ago.

Sure, everyone probably needs some stocks in their portfolio in retirement. Returns from cash and bonds may not keep up with inflation, after all, but stock returns might fall short too and, if stocks do lag, they probably won’t do so with the limited volatility that bonds tend to deliver, barring a serious bout of inflation.

Bottom line:

If you’re within a decade of retirement, it may be time to think hard about how much stock exposure is enough. The answer might be less than you think for a portfolio in distribution phase.

If you enjoyed the above article sign up in the top right hand corner of this page and receive our FREE bi-weekly newsletter (see sample here)

(*The author’s views and conclusions are unaltered and no personal comments have been included to maintain the integrity of the original article. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor.)

Related Articles From the munKNEE Vault:

1. Don’t Use the 4% and 60-40 Investing Rules of Thumb – They’re Dumb! Here’s Why

One of the things that really frosts me is the financial planning industry that insists on using rules of thumb such as the “set and forget” tools – specifically the 4% and 60-40 rules.

2. Use The 4% Rule To Thrive In Retirement – Here’s How

This post looks at the 4% rule to understand why it works so well in retirement, what could possibly be a stumbling block and how to overcome such a situation should it arise.